Philippines lags ASEAN neighbors in FDI Confidence Index

By Justine Irish D. Tabile, Senior Reporter

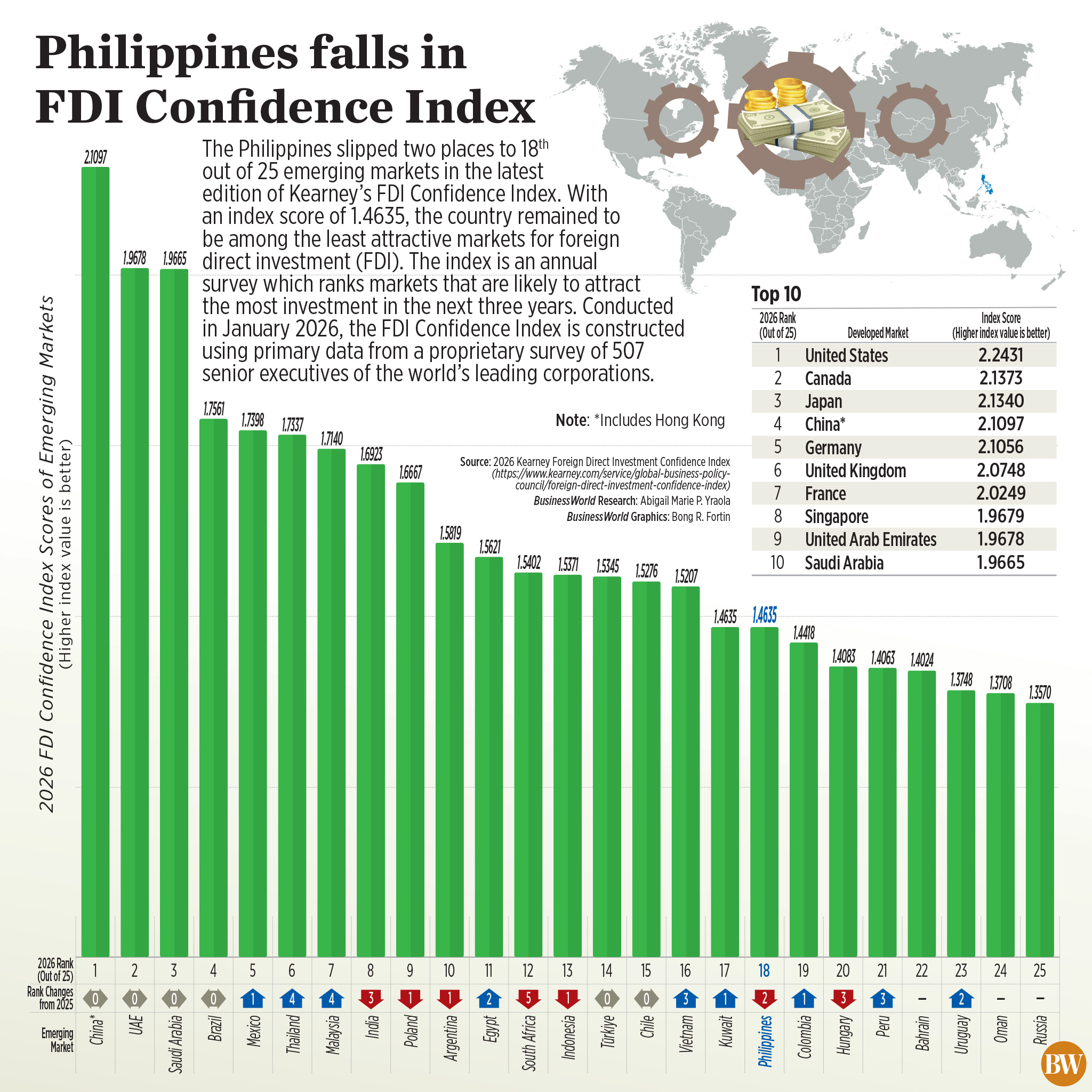

THE PHILIPPINES dropped two spots to 18th out of 25 emerging markets in the 2026 Foreign Direct Investment (FDI) Confidence Index by global management consulting firm Kearney.

The Philippines posted a score of 1.4635 in the index, which ranks markets that are likely to attract the most FDI in the next three years.

This was the third straight year the Philippines’ ranking declined in the index. It ranked 16th in 2025, 13th in 2024 and 12th in 2023.

“The index reflects a three-year outlook, so the shift points to softer medium-term investor confidence, rather than any single short-term factor,” Kearney Senior Partner, Philippines Country Head & APAC Communications, Media & Technology Lead Marco de la Rosa said in an e-mail interview.

“At the same time, recent Philippine-specific developments, including headlines last year around infrastructure spending and political challenges, may have weighed on investor sentiment, alongside a more risk-sensitive global environment, making the country a relatively less attractive destination for FDI,” he added.

The Philippines was rocked by a corruption scandal last year that linked government officials, lawmakers, and public contractors to anomalous flood control projects.

In 2025, the Philippines saw its FDI net inflows drop 17.1% year on year to $7.791 billion. This was the lowest yearly FDI level since 2020.

The downtrend continued at the start of this year as January FDI net inflows slid to a four‑month low of $443 million, 39.2% lower compared with the same month a year ago.

Conducted in January 2026, the FDI Confidence Index uses primary data from a proprietary survey of 507 senior executives of the world’s top corporations.

“China, the United Arab Emirates, and Saudi Arabia lead the emerging market ranking for the third consecutive year,” Kearney said.

Among emerging markets, the Philippines fell behind regional peers such as Thailand (6th), Malaysia (7th), Indonesia (13th) and Vietnam (16th).

“Other ASEAN (Association of Southeast Asian Nations) markets have become more attractive, particularly those benefiting from supply chain shifts and stronger positioning in innovation,” Mr. de la Rosa said. “Thailand and Malaysia are benefiting from China+1 diversification, while Vietnam stands out for linking talent to a clear sector strategy, particularly in semiconductors.”

Ateneo Center for Economic Research and Development Director Ser Percival K. Peña-Reyes said that the steady decline in the index is not driven by a single factor but rather by the Philippines’ relative underperformance versus peers and persistent structural constraints.

“The index is relative, so even if the Philippines is stable, (the fact) that other countries are rising faster pushes it down,” he said in a Facebook Messenger chat.

According to Kearney, investors cited the Philippines’ labor talent as its strongest asset (32%), followed by natural resources (28%) and economic performance (27%).

A fourth of the investors have identified the country’s tech innovation and ease of doing business as top reasons for investments, while 22% cited transparent governance. Only 12% cited infrastructure quality.

However, a small percentage or 2% said that there were no strong reasons at all to invest in the Philippines.

“What it suggests is that, for a small group of investors, the Philippines’ strengths may not yet be coming through as distinctly as some peers,” Mr. de la Rosa said.

Mr. Peña-Reyes said that the country continues to show weaknesses in the areas that investors are focusing on.

“Our innovation ecosystem is still lagging versus our peers. Our bureaucracy and regulatory complexity remain huge concerns. Our infrastructure gaps persist despite improvements,” he said. “Nevertheless, if the Philippines improves execution, specialization, and policy clarity, it can realistically reverse the trend within a few years.”

Mr. Peña-Reyes said that the Philippines can no longer rely on its talent pool, as other countries are highly competitive. For instance, 40% of investors view India’s talent pool as its strongest asset, while 34% cited the same for Vietnam.

“To stay competitive, [the Philippines] needs to differentiate, upgrade, and support talent. If it does these things well, it can remain highly attractive, even against larger players like India and fast-rising ones like Vietnam,” he said.

The survey showed investor sentiment in the Philippines had a score of -2, with 22% pessimistic about the Philippines’ three-year economic outlook compared with 20% optimistic.

Two other countries with negative optimism scores were Malaysia and Russia, which had -7 and -10, respectively.

“For the Philippines, the implication is clear. Even if its talent advantage remains strong, it must reduce uncertainty, improve execution, and signal stability to convert interest into actual inflows,” Mr. Peña-Reyes said.

While the survey was conducted before the Iran war, Kearney said investors already expected an increase in geopolitical tensions (36%), a rise in commodity prices (30%), and political instability in a developed market (30%) to occur in the next year.

“When the survey was in the field in January, there was incredible instability in the global operating environment that likely drove a rise in geopolitical tensions to the top of the rankings,” Kearney said.

The report pointed to global instability, citing military operations in Venezuela, protests in Iran, and reports about the US potentially using force to acquire Greenland.

Kearney said that these tensions are likely to have contributed to greater concerns over increased political instability and rising commodity prices “which often occurs amid conflict-induced supply chain disruptions, as in the current Middle East conflict.”

Meanwhile, Kearney said that industrial policy is becoming an extremely important determinant in where investors put their investments, especially for information technology, heavy industry, telecommunication sectors, and healthcare firms.

“Investors recognize industrial policy as an important factor in making FDI decisions: 84% say industrial policy is “extremely” or “very” important,” it said.

“Predictability, grounded in clear and consistent industry policy frameworks, is key to sustaining investor confidence and strengthening industrial policy outcomes,” it added.

In particular, the report identified infrastructure development (80%) and tax incentives (78%) as the most positively viewed industrial policy tools.